http://www.freep.com/article/20110329/BUSINESS04/103290329/In-Detroit-urban-farming-waiting-take-root

Friday, April 29, 2011

Pictures anyone?

See here. I want to learn how to use google maps to make pictures like this. But they are so horrifying, I am not sure why.

Thursday, April 28, 2011

Land bank fights blight: $15 million program to return property to tax rolls

This article includes what Kalamazoo has been doing to deal with foreclosure and abandonment. Some of the things were mentioned during the presentation in the class on Thursday.

Las Vegas Abandoned Houses

I am posting this article because it brings up an interesting question about banks. How can we hold banks and owners of property accountable for dilapidated, foreclosed homes even if it means to demolish some of them?

Shrinking cities

Shrinking cities are a problem across the country and Baltimore is no exception. This article outlines a few of Baltimore's current initiatives and suggests a few that are being tested in other cities such as Cleveland and Philadelphia.

The comments at the end of the article list a number of different strategies for dealing with abandoned or vacant properties. I like how the first comment points out that there are different strategies being tested in a number of neighborhoods and it is this response to specific neighborhood needs that will really make these programs successful.

Also, take a look at the last comment, "Nature Reclaims Land." There are some shocking pictures tagged at the end of the comment.

Sputnik Moments

After reading Adam’s post, I started thinking about the history and future of the government’s role in higher education and funding, and tried to make some comparisons and contrasts.

Feeling outdone by the Russians in 1957, the US government became increasingly interested in investing in students, in giving students a competitive edge in the market, and ultimately giving the country a competitive edge within the world economy. In this way, the original goal of the government was to try to make higher education more accessible, regardless of what families could afford – that’s the key phrase. It seems noble in intention, but is creating a bubble and saddling students with an enormous burden.

I am less critical of Obama’s State of the Union rhetoric in light of the bill he signed to overhaul the student loan program. He spoke of the United States’ “Sputnik moment” and the need to “invest in the future.” Drawing historical parallels, his statement was largely interpreted according to our previous “Sputnik moment,” the one that spurred the development of the bank-based student loan program in 1965. Obama’s mission, however, has been to restructure and monitor that system. Moreover, the bill’s purpose was to restructure the system of financial aid in a way that would minimize the burden of debt for lower-income student seeking higher education. It “eliminates fees paid to private banks to act as intermediaries in providing loans to college students and use much of the nearly $68 billion in savings over 11 years to expand Pell grants and make it easier for students to repay outstanding loans after graduating.” It also allows students to “to cap repayments at 10 percent of income above a basic living allowance, instead of 15 percent. Moreover, if they keep up payments, their balances will be forgiven after 20 years instead of 25 years — or after 10 years if they are in public service, like teaching, nursing or serving in the military.” The greatest triumph, however, was in calling out Sallie Mae, which has “received guaranteed federal subsidies [since 1965] to lend money to students, with the government assuming nearly all the risk.” The program essentially “fattened the bottom line for banks AT THE EXPENSE OF STUDENTS AND TAXPAYERS. Why are we paying people to lend the government’s money and then the government guarantees the loan and the government takes back the loan?” Sounds familiar. It’s very telling, and frightening, the extent to which Sallie Mae pervasively has its hands in every corner of the economic crisis. At the same time, it’s somewhat uplifting to see Obama and legislators going after Sallie Mae, even if bills are watered down considerably in Congress, and even if it is done in the context of competing with China.

http://www.nytimes.com/2010/03/26/us/politics/26loans.html

http://www.nytimes.com/2010/03/31/us/politics/31obama.html

Is student debt the next bubble?

http://nplusonemag.com/bad-education

This is something a friend showed me. The article is particularly relevant to our class because it compares student loan debts with the subprime crisis to predict what would happen if the bubble burst. The whole thing is pretty interesting, but here are some high points:

"Last August, student loans surpassed credit cards as the nation’s single largest source of debt, edging ever closer to $1 trillion.... Since 1978, the price of tuition at US colleges has increased over 900 percent, 650 points above inflation. To put that number in perspective, housing prices, the bubble that nearly burst the US economy, then the global one, increased only fifty points above the Consumer Price Index during those years"

"the Student Loan Asset-Backed Securities (SLABS) were invented by then-semi-public Sallie Mae in the early ’90s, and their trading grew as part of the larger asset-backed security wave that peaked in 2007."

And this was particularly troubling to me: "What analysts at Barclays Capital wrote of the securities in 2006 still rings true: “For this sector, we expect sustainable growth in new issuance volume as the growth in education costs continues to outpace increases in family incomes, grants, and federal loans.” "

It's like they're saying its a bubble, and don't even realize they're saying it. What do you think? Is an education worth the $160,000 or so K is charging?

Wednesday, April 27, 2011

Dave Bing on Fixing Detroit

Does this bear a striking resemblance to the situation in Cleveland? Detroit lost 25% of their population between 2000 and 2010. Going from a city of 900,000 to 713,000. Cleveland only lost 17% of their population in the last 10 years. However both are historic. Detroit had the auto industry, while Cleveland had the steel industry. Both industries had good paying jobs that required minimal education.

Both face issues of abandonment and vacancies. Neither have the tax base or the resources to combat this issue. So what do you think, can either city be brought back?

http://www.businessweek.com/magazine/content/11_18/b4226096954910.htm

Abandoned houses require team effort

Team effort: One way to deal with abandonment.

http://pharostribune.com/editorials/x2095869694/Abandoned-houses-require-team-effort

http://pharostribune.com/editorials/x2095869694/Abandoned-houses-require-team-effort

Tuesday, April 26, 2011

Kalamazoo powerpoint on NSP program

I don't know why I couldn't get this up in class. But here is the link. Look at it before Thursday if you would. Thanks.

http://www.kalamazoocity.org/docs/NSP2Slideshow042210.pdf

http://www.kalamazoocity.org/docs/NSP2Slideshow042210.pdf

Why is the abandonment problem hard to solve?

This article talks all about Abandoned buildings and has a lot of great stuff, but I want you all to look at part 3 section i) which deals with trying to tackle the abandonment problem. Abandonment is not a relatively new issue, however it has never been solved.

One of the main problems is that there are many economic and legal obstacles when dealing with abandonment. As we have seen with this whole housing crisis, obstacles are always difficult to deal with and often lead to fraud and more issues.

What solutions can be found for the abandonment issue? How can the community get involved? What should the government be doing to solve this issue?

Pressure on Banks

Are they stepping up regulation? Or is this just symbolic?

http://www.economist.com/node/18586826?story_id=18586826

http://www.nytimes.com/2011/04/15/business/15market.html?_r=2&scp=1&sq=mortgage%20crisis&st=cse

http://www.economist.com/node/18586826?story_id=18586826

http://www.nytimes.com/2011/04/15/business/15market.html?_r=2&scp=1&sq=mortgage%20crisis&st=cse

“Foreclosed: Rehousing the American Dream”

An interesting project and perspective.

http://www.nytimes.com/2011/04/25/arts/design/moma-competition-seeks-better-american-housing.html?scp=2&sq=foreclosure%20crisis&st=cse

http://www.nytimes.com/2011/04/25/arts/design/moma-competition-seeks-better-american-housing.html?scp=2&sq=foreclosure%20crisis&st=cse

Monday, April 25, 2011

Abandoned buildings pose health, safety risks

Here are some problems caused due to housing abandonment. It's an example of how a community was affected due to abandoned buildings. However it does not give a detail explanation about the problems associated with abandonment.

http://www.dailytexanonline.com/content/abandoned-buildings-pose-health-safety-risks

How would you revitalize Detroit?

This is one of the million dollar questions. How do you revitalize? Detroit is just one of the many facing problems due to abandonment, financial issues and unemployment. The conference held at the Westin Book Cadillac hotel in Detroit brainstormed ideas for revitalizing cities like Detroit.

What do you think of the ideas proposed? Should these ideas be applied to all cities or just the ones facing hardships?

One solution to solve the abandonment problem

This article I found does not have all the answers, nor does anyone else, however it gives some insight on what we need to do in order to fix the problem of abandoned homes. The main point that I drew from this article is that one cannot rely solely on the government or a group of people to fix all of our problems; people need to work together as communities, partnered with the government and private groups, to fix this mess.

Timeline of the Crisis

http://motherjones.com/politics/2008/07/where-credit-due-timeline-mortgage-crisis

I found this timeline to be really interesting and useful. It gets into some of the historical precedents that lead up to the crisis, which helped give more background and context.

What do you guys think? Does anything on the timeline surprise you?

I found this timeline to be really interesting and useful. It gets into some of the historical precedents that lead up to the crisis, which helped give more background and context.

What do you guys think? Does anything on the timeline surprise you?

Money and Property Waiting to be Claimed

I found this CBS article and in it you can watch a short video about the fact that the State of Illinois has over 1 billion dollars just waiting to be claimed. When I read this article, I was constantly thinking about how uneducated people are during this economic "depression." Let me know what you all think.

Sunday, April 24, 2011

Balance the Budget

Want to balance Michigan's budget, then go to the following link. http://www.thecenterformichigan.net/you-balance-the-state-budget/

This simulator allows you to make the tough choices. Once you're finished you can share your results with your friends. It gives you a look at the top five proposals in order of size and then shows you your top five proposals.

Do you think it is as easy as it looks?

Have we abandoned the American Dream of home ownership?

Read the following article Home Ownership Luster Fading in U.S. from the Detroit News and tell us what you think. http://detnews.com/article/20110420/BIZ/104200328

With a decline in housing prices, people underwater in mortgages and the housing crisis being related back to the Great Depression have we lost our faith in real estate?

Perspectives on Economy and Labor

The Economist has a good section up where various guests (generally professors and experts from around the country) post answers on a theme. One of the current ones is on "What's wrong with America's labor market?" and the answers range from a discussion of how mortgage uncertainty hurts the entire workforce by decreasing our liquidity as a nation to an argument that frankly there hasn't been a recovery yet.

The sections are short, quick reads and very thought provoking. What do you make of the various points? IS there any one that seems most relevant to our class? In "Housing problems leave workers stuck," the author makes a suggestion at the end that seems like it would be almost impossible politically, but may be the right choice economically... Is it one that's worth exploring?

The sections are short, quick reads and very thought provoking. What do you make of the various points? IS there any one that seems most relevant to our class? In "Housing problems leave workers stuck," the author makes a suggestion at the end that seems like it would be almost impossible politically, but may be the right choice economically... Is it one that's worth exploring?

Friday, April 22, 2011

Michigan FTW

The most surprising thing in reading this article on rebalancing housing in the economy was that housing prices nationwide are only down 18.5% from their peak. Not that 18.5% isn't a huge loss, but when we looked up tax data after the city survey it seemed like for our neighborhood at least, which was pretty much working class/lower middle class, housing values were down about 50%.

The article goes onto cite Detroit and Grand Rapids as two particularly hard hit markets, and Kalamazoo could be added to that list. It seems like Michigan never catches a break, economically speaking.

The conclusion is one of the more cogent statements of where housing policy and economics went wrong and what has to be done to keep things in better line as the economy recovers. The Great Recession is compared to the Great Depression in that it is a turning point: things simply can't go back to 'the way they were.'

When you collected tax data, how much had your properties fallen in value? And how common were sales since 2006 or so, when the crash started?

Allen Mallach's Thoughts on Improving Detroit

http://wgisblog.com/2010/03/13/how-would-you-revitalize-detroit/

What a crazy chart...

The pricing information in this article shouldn't be too shocking this late into our class, but it's interesting to see it presented quantitatively and the graph is pretty striking.

The second half of the block quote is pretty incendiary though:

"Instead of allowing the housing market to correct to its fair value, President Obama and Barney Frank will attempt to “mitigate” foreclosures. Mr. Frank has big plans for your tax dollars, "We may need more than $50 billion for foreclosure [mitigation]". What this means is that you will be making your monthly mortgage payment and in addition you will be making a $100 payment per month for a deadbeat who bought more house than they could afford, is still watching a 52 inch HDTV, still eating in their perfect kitchens with granite countertops and stainless steel appliances."

What do you think of this position? I tend to agree that housing prices still have a long way to fall, but I also see keeping people in houses as a good for slowing that transition, which has some benefits. I would also dtend to say the externalities on keeping people in houses probably covers some of the cost of helping them with mortgages, but it'd be interesting to see a study on the general economic result of a foreclosure.

Anyways, where do you stand on programs to keep people in houses they can't afford at taxpayer expense?

Corruption or fund-raising expertise: you decide

Matt Taibbi, one of the best, although colorful, investigative reporters of all things financial, has taken a look at the lead negoitiator for the state attorney generals. He says

"A hilarious report has come out courtesy of the National Institute of Money in State Politics, showing that Iowa Attorney General Tom Miller – who is coordinating the investigation into the banks’ improper mortgage dealings – increased his campaign contributions from the finance sector this year by a factor of 88! He has raised $261,445 from finance, insurance and real estate contributors since he announced that he was going to be coordinating the investigation into improper foreclosure practices. That is 88 times as much as they gave him not over last year, but over the previous decade. "

He calls it "hilarious;" I call it frightening and sad.

Thursday, April 21, 2011

MERS: Stop Foreclosing in Our Name

Read this first for a little bit to get the gist of it.

Then, bam. Read this article!

Haha, I kind of find it interesting on what MERS is doing. They are telling people to stop foreclosing in MERS' name.

Sounds like they're trying to save themselves, don't ya think? Do you think that even now we are letting them getting away from it?

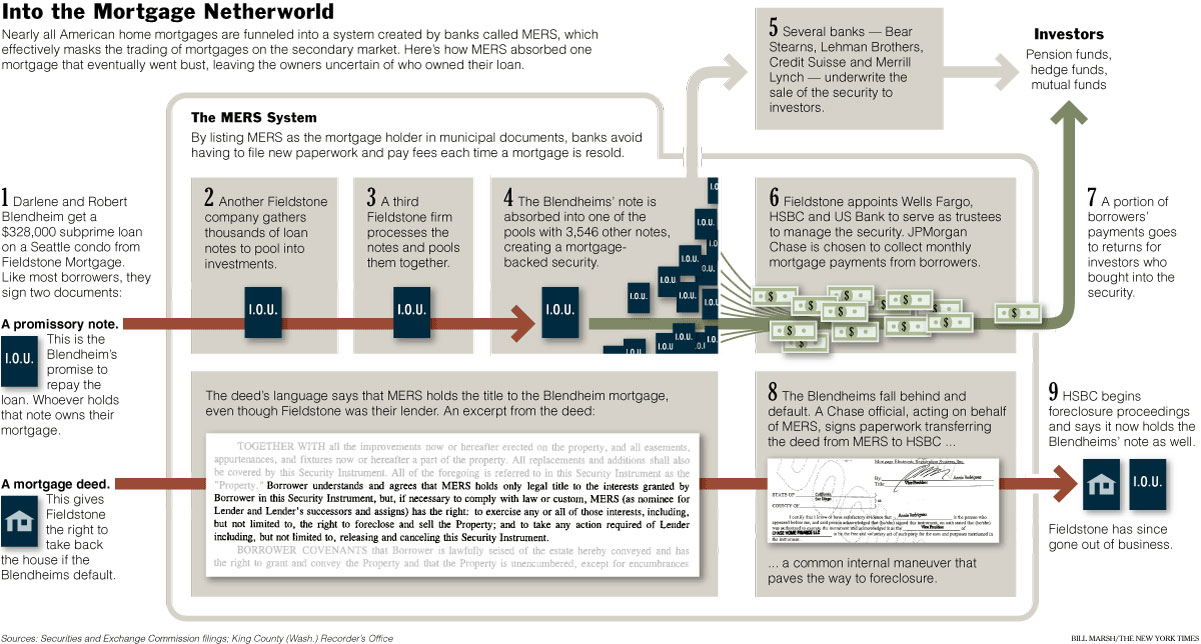

MERS - a hot mess of the mortgage world

Our group just spent the past hour or so trying to figure out what the heck MERS is and the most succinct conclusion we can really make is that it's a company that designed to be a very deliberate deception of American homeowners. Here's a detailed flow chart to help unpack and organize some of the different properties of MERS that might help prep you for our PowerPoint presentation on the company next Monday. Click here for a larger image.

{kind=link}

Let us know what questions you have so we can look into them a little more before we present! Opinions are appreciated as well.

I'm curious

In this cycle of Republican rhetoric for less "big government", lower taxes, and the prevailing sentiment that the states should be better able to take care of themselves, am I the only one who thought it ironic that the Governor of Texas is seeking Federal funds to help cover the cost of disaster relief in his state? Maybe I'm wrong and off-base, I just thought I would put it out there.

Wednesday, April 20, 2011

http://www.businessinsider.com/the-housing-chart-thats-worth-1000-words-2009-2

This article presents an interesting, though strongly stated, view on housing prices. The author argues that there needs to be less focus on bringing housing prices back up and criticizes the factors that caused the housing bubble in the first place.

Thoughts?

This article presents an interesting, though strongly stated, view on housing prices. The author argues that there needs to be less focus on bringing housing prices back up and criticizes the factors that caused the housing bubble in the first place.

Thoughts?

Home sales up, but...

An article in the Detroit Free Press notes that there was a 3.7% increase from February to March in home sales in the U.S. This is not yet at the levels most economists say are necessary for a healthy economy, but increase is good, right?

Unfortunately, this is a case where the whole story is very different from those first numbers. 35% of those homes sold were paid for in full, in cash...Home sales rose 3.7 NATIONALLY, but that breaks down into an 8.2% increase in the South and only a 1% increase in the Midwest... This means that a large % of those encouraging home sales are actually investments and not homes being bought by individuals or families.

Even beyond that, these statistics admit they don't take homes sold in bulk into account, meaning that large private investment firms buying up large numbers of foreclosed properties need to be added on to these totals.

So, home sales are up, but... more as economic opportunities manifesting for people and organizations who are already wealthy, as opposed to for individual Americans pursuing the "American Dream" of owning a home.

So, is this good? It certainly isn't a bad thing that home sales are going up and stimulating the economy. But is it bad for individual owners? Large numbers of sales of foreclosed homes drive down the price of all homes, hurting owners who avoided foreclosure by reducing the value of their investment.

Also, this increase is very heavily weighted toward the areas of the country where foreclosure hit hardest- is that good because it is helping the hardest hit areas, or bad because it is simply outside business taking advantage of a bad situation?

Unfortunately, this is a case where the whole story is very different from those first numbers. 35% of those homes sold were paid for in full, in cash...Home sales rose 3.7 NATIONALLY, but that breaks down into an 8.2% increase in the South and only a 1% increase in the Midwest... This means that a large % of those encouraging home sales are actually investments and not homes being bought by individuals or families.

Even beyond that, these statistics admit they don't take homes sold in bulk into account, meaning that large private investment firms buying up large numbers of foreclosed properties need to be added on to these totals.

So, home sales are up, but... more as economic opportunities manifesting for people and organizations who are already wealthy, as opposed to for individual Americans pursuing the "American Dream" of owning a home.

So, is this good? It certainly isn't a bad thing that home sales are going up and stimulating the economy. But is it bad for individual owners? Large numbers of sales of foreclosed homes drive down the price of all homes, hurting owners who avoided foreclosure by reducing the value of their investment.

Also, this increase is very heavily weighted toward the areas of the country where foreclosure hit hardest- is that good because it is helping the hardest hit areas, or bad because it is simply outside business taking advantage of a bad situation?

Tuesday, April 19, 2011

Winner of Google's Data Viz Challenge for Visualizing Tax Data

In February, Google challenged its users to present tax data in an exciting way, utilizing video, graphics, and text to turn information into understanding. Out of over 40 projects, Google chose Anil Kandangath and his site Where Did My Tax Dollars Go? as the winner. This site breaks down your tax payments into a pie chart and a flow chart, showing you dollar for dollar where your money went.

If you use the equation that the site prompts you with (paying $5000 and filing as "single"), you end up contributing $54 to community and regional development and $111 for commerce and housing credits, which are some of the smallest fractions of the pie chart. Do you feel like your money is being allocated in the correct way?

Obama Housing Plan

http://topics.nytimes.com/top/reference/timestopics/subjects/c/credit_crisis/housing_plan/index.html?scp=10&sq=housing%20&st=cse

This article describes a program that Obama initiated in light of the foreclosure crisis to help keep people in their homes.

The article gets into some of the elements that caused the program to lack effectiveness and eventually lead to its cancellation last month.

What do people think of these varying factors that impeded the program's success? I personally found the mistakes/ misinformation from the banks to be appalling.

This article describes a program that Obama initiated in light of the foreclosure crisis to help keep people in their homes.

The article gets into some of the elements that caused the program to lack effectiveness and eventually lead to its cancellation last month.

What do people think of these varying factors that impeded the program's success? I personally found the mistakes/ misinformation from the banks to be appalling.

Proposed Foreclosure Law

http://www.mlive.com/news/index.ssf/2011/04/does_proposed_michigan_foreclo.html

I just found this article, from the Grand Rapids Press, about the new proposed foreclosure law in Michigan. The law proposes shortening the redemption period from 6 months to 3. What does everyone else think of this? Is this really the best way to go about dealing with the foreclosure crisis? Personally, I don't see it helping things, because what most people need when they're at risk of foreclosure is more time to get their finances back on track.

"Michigan and Ohio are even worse"

This article, entitled "This is why we're broke" doesn't directly address foreclosures, but it's hard not to see the link between exurbanization, the housing boom and all the new development it created. The costs of home ownership are not only in the home itself and as Aaron Renn points out, suburbs are really expensive, especially if the people moving to them from the central city in a region. This is making our governments broke, but it seems to me that its pretty analogous to why so many families are broke these days.

The boom resulted in more people moving to more expensive housing with higher carrying costs without the underlying economic growth to support the increased costs. This article suggests a similar bubble bursting could be coming for state governments.

What do you think? Particularly about his final paragraph:

"I’m not saying we should ban people from moving to the exurbs in stagnant or declining regions, but at a minimum it should be made very clear to those who do that they have to pay 100% of the freight on their own, and that no state or federal funds are going to be expended in support of that."

As an aside, Aaron Renn/Urbanophile is about the best urbanist writing I've found, I'd really recommend reading it regularly if you have any interest in cities, urban policy or urban economics

Monday, April 18, 2011

Less than Optimistic

http://www.msnbc.msn.com/id/42644103/ns/business-eye_on_the_economy/

http://www.oregonlive.com/business/index.ssf/2011/04/home_builders_sentiment_more_p.html

For reference a rating above 50 indicates a favorable outlook on home sales, below indicates a negative outlook.

This suggests that the outlook for housing is only getting worse. This does not bode well for those individuals hoping to have their home appreciate in value anytime soon. Home building is like a self-perpetuating cycle in that the reasons individuals don't buy homes (i.e. loss of job) increases the number of others who don't buy homes (very poor English).

What I am trying to say is that home building creates on average 3 jobs per house. By individuals not purchasing homes it is further preventing others from purchasing homes in terms of a new house not being built.

A good quote from one of the articles "High unemployment, tighter lending standards and bigger requirements for down-payments are keeping many people from buying homes. A record number of foreclosures are forcing down home prices, leaving would-be buyers worried that the market has yet to bottom out."

Thoughts?

http://www.oregonlive.com/business/index.ssf/2011/04/home_builders_sentiment_more_p.html

For reference a rating above 50 indicates a favorable outlook on home sales, below indicates a negative outlook.

This suggests that the outlook for housing is only getting worse. This does not bode well for those individuals hoping to have their home appreciate in value anytime soon. Home building is like a self-perpetuating cycle in that the reasons individuals don't buy homes (i.e. loss of job) increases the number of others who don't buy homes (very poor English).

What I am trying to say is that home building creates on average 3 jobs per house. By individuals not purchasing homes it is further preventing others from purchasing homes in terms of a new house not being built.

A good quote from one of the articles "High unemployment, tighter lending standards and bigger requirements for down-payments are keeping many people from buying homes. A record number of foreclosures are forcing down home prices, leaving would-be buyers worried that the market has yet to bottom out."

Thoughts?

How To Save A Trillion Dollars

A billion dollars isn't cool. You know what's cool? A trillion dollars. That's the point this NY Times article is making about a relatively easy way for the U.S. to save over a trillion dollars in costs (as much as saving a trillion dollars is ever easy).

Interesting.

"Lifestyle diseases" are diseases that are caused by controllable factors in your daily life: diabetes, heart disease, some cancer, etc. In some cases these are more than "lifestyle" and you simply have bad genetic luck; in others, you are getting these diseases only because of your (bad) individual choices in terms of athletic activity, good diet, and mental health. Treating these diseases now takes up more than 1/7 of our national GDP. And that's TREATING, as in dealing with symptoms and not the underlying cause. The point, of course, is that by changing our basic eating habits to be even a bit more healthy and exercising a little more as a nation, we could be saving ourselves amounts of $$ that would be counted in terms of hundreds of billions.

How does this relate to urban econ? To me, it ties very closely into at least two articles we've already looked at, about new urban grocery stores and about health conditions in urban settings. One way the government could be saving money on a massive scale would be through funding smaller, healthier food options, especially in urban settings (e.g. more organic type sections in markets, generous grants to small businesses who sell food that meets a certain health standard, more attention to creating healthy meals and eating patterns in public schools). This would have pretty immediate and tangible financial results.

Thoughts? Other ways the government could try and influence the conditions that cause these lifestyle diseases? Would it be better for efforts towards that to come from local, state, or federal government?

Interesting.

"Lifestyle diseases" are diseases that are caused by controllable factors in your daily life: diabetes, heart disease, some cancer, etc. In some cases these are more than "lifestyle" and you simply have bad genetic luck; in others, you are getting these diseases only because of your (bad) individual choices in terms of athletic activity, good diet, and mental health. Treating these diseases now takes up more than 1/7 of our national GDP. And that's TREATING, as in dealing with symptoms and not the underlying cause. The point, of course, is that by changing our basic eating habits to be even a bit more healthy and exercising a little more as a nation, we could be saving ourselves amounts of $$ that would be counted in terms of hundreds of billions.

How does this relate to urban econ? To me, it ties very closely into at least two articles we've already looked at, about new urban grocery stores and about health conditions in urban settings. One way the government could be saving money on a massive scale would be through funding smaller, healthier food options, especially in urban settings (e.g. more organic type sections in markets, generous grants to small businesses who sell food that meets a certain health standard, more attention to creating healthy meals and eating patterns in public schools). This would have pretty immediate and tangible financial results.

Thoughts? Other ways the government could try and influence the conditions that cause these lifestyle diseases? Would it be better for efforts towards that to come from local, state, or federal government?

Sunday, April 17, 2011

Powerpoint Presentation from Tuesday's Class

To use as a reference. This is especially for editing the white paper for last week's class. Here's the link to the Google Doc for it.

Great Website for your Housing Market/Foreclosure Needs

http://www.reuters.com/subjects/housing-market

While surfing the internet today for my new blog post I came across the web page above on Reuters. I thought it was great because it compiles tons of news articles relevant to the housing market.

This article caught my attention, it is a little lengthy but a good read none the less. The article talks about a decree that "Call[s] for stricter rules for handling mortgage documentation, better procedures for dealing with homeowners, internal investigations, and restitution to some homeowners if evidence shows that foreclosures were carried out in error." Unfortunately, all the major banks seem to be dragging their feet and prolonging such negotiations.

Thoughts?

While surfing the internet today for my new blog post I came across the web page above on Reuters. I thought it was great because it compiles tons of news articles relevant to the housing market.

This article caught my attention, it is a little lengthy but a good read none the less. The article talks about a decree that "Call[s] for stricter rules for handling mortgage documentation, better procedures for dealing with homeowners, internal investigations, and restitution to some homeowners if evidence shows that foreclosures were carried out in error." Unfortunately, all the major banks seem to be dragging their feet and prolonging such negotiations.

Thoughts?

Saturday, April 16, 2011

Photos from Housing Survey

Our group took photos from our housing survey in the north Portage commercial/residential area. View the full album here.

Guys, I have a new hobby! I like to flip houses!

http://articles.chicagotribune.com/2011-04-15/classified/sc-cons-0414-foreclosure-flippers-20110415_1_foreclosure-properties-foreclosure-auction-low-p

Read this recent article (3 pages), and see how disturbing it is to buy other people's homes or take advantage of other people's losses.

Any thoughts?

If you were in a same position like this guy, would you do it to make profits?

Rising Prices and their Effects

http://finance.yahoo.com/news/Consumers-feel-the-pinch-of-apf-3014714615.html?x=0&sec=topStories&pos=5&asset=&ccode=

Although not directly related to foreclosures I will attempt to bridge the two. This article talks about the effects of rising food and gas prices throughout the United States. While the rise in these prices has not spread to other items the consumer is definitely seeing the effects. When essentials like food and gas increase in price the cost of living obviously increases.

As a result of said increases do you think we will see an increase in foreclosures, as consumers will now be more strapped for cash? In my opinion the resulting changes are too minute to have any dramatic effects.

Thoughts?

Although not directly related to foreclosures I will attempt to bridge the two. This article talks about the effects of rising food and gas prices throughout the United States. While the rise in these prices has not spread to other items the consumer is definitely seeing the effects. When essentials like food and gas increase in price the cost of living obviously increases.

As a result of said increases do you think we will see an increase in foreclosures, as consumers will now be more strapped for cash? In my opinion the resulting changes are too minute to have any dramatic effects.

Thoughts?

Response to Foreclosure Nation

This week we have attempted to focus on a very specific topic, foreclosures and Kalamazoo. We have also just finished reading the book Foreclosure Nation. We haven't had much of an opportunity to discuss the book in class so I want to post this question.

What is your response to the book?

Overall I thought the book was an interesting read. I found the chapters full of definitions helpful and enlightening but I am afraid I will not remember much of them after a week (at least now I know where to look if I ever hear an unfamiliar term). The author brings up a lot of thought provoking questions in the final chapter, which I enjoyed the most.

What is your response to the book?

Overall I thought the book was an interesting read. I found the chapters full of definitions helpful and enlightening but I am afraid I will not remember much of them after a week (at least now I know where to look if I ever hear an unfamiliar term). The author brings up a lot of thought provoking questions in the final chapter, which I enjoyed the most.

Thursday, April 14, 2011

Kalamazoo Neighborhood Services Inc.

http://knhs.org/

http://www.northsidenacd.com/

For those of you that are interested in learning more about organizations that help people deal with foreclosures in Kalamazoo, feel free to check out those sites.

Outline

Everyone, please put something on our outline in Google!!!

https://docs.google.com/document/d/1HDQcmmkaHlpziri2MOzSdjKoIndjZu2F2rtRIVcZRDk/edit?hl=en#

Please don't forget it!

Thank you!!!

Paul A. Garza K'12

Tour de K

After a grueling day rating homes I am interested to hear some reactions. Most of the homes in my groups area ranked houses in the 4-6 range with a couple 1-3s thrown into the mix. One thing that I noticed however was that my home ranking scale seemed to change while I was in this neighborhood. For example, a home I normally would call a 4 became a 6 when I compared it to surrounding homes. Also, I found myself being bias to home selection. If we drove past a particularly gruesome home it had to be rated. However, if we drove past a "nicer" home for this particular area I felt we were less likely to rate it.

What did the other groups think? Did you find anything shocking, disturbing?

What did the other groups think? Did you find anything shocking, disturbing?

Wednesday, April 13, 2011

Vacancy

Here is a link to a map showing vacant homes and businesses throughout the US. You can zoom in on Michigan and have a better look at Kalmazoo. We are actually doing better than most other counties in Michigan with residential vacancy at 3% and business vacancy at 11%. Unfortunately, looking at the map that depicts change from quarter to quarter these numbers seem to be slightly increasing.

Why do you think Kalamazoo is "becoming more vacant" and what types of things can the city do to help alleviate the problem.

Why do you think Kalamazoo is "becoming more vacant" and what types of things can the city do to help alleviate the problem.

Pre Crisis Hindsight

This link provides access to the Chicago Fed page where there are links to download various powerpoint presentations. Each one has different graphs of the mid west and provides different data from 2007 and later. I found them really interesting as you can look at the state of Michigan pre-crisis. When you compare these graphs to ones post crisis you can see the correlation between foreclosures today and high cost sub prime lending in the past.

Kalamazoo Neighborhood Housing Services Grant

http://www.mlive.com/news/kalamazoo/index.ssf/2011/01/100000_raised_for_foreclosure-.html

Here's an article that gives some more information about one of the local programs Chris mentioned in our presentation on Tuesday. The $100,000 grant, which was approved in Jan/Feb 2011, was made possible by money raised by the Kalamazoo Neighborhood Housing Services. The grant is intended to provide one-time help to Kalamazoo homeowners, who can receive up to $2,000 to help with mortgage payments and avoid foreclosure.

Monday, April 11, 2011

Economists to Follow on Twitter

You got your flashy new Twitter handle last week - now who do you follow? Here are a few suggestions to get some awesome economics-related Tweets in your feed:

- The Economist

- Freakonomics

- NYTimesBusiness

- WSJ_Econ

- Nouriel (Nouriel Roubini)

- Bill_Easterly

Funny "Real Estate Downfall" Video

Okay, I know, I know. This video is pretty silly. But for those like me who felt like reading about the real estate market collapse was like reading in a foreign language (German, perhaps?), it's actually really rewarding to watch this video because if you've done the reading you can actually understand most if not all of the real estate references they make. A few of the buzz phrases I caught include:

- Adjustable rate mortgage

- McMansion

- Housing bubble

- Refinance

- Home equity loan

- "Pick a payment"

- Lehman/AIG stock

- Government bail out

It's a ridiculous video, but it's also a good test of your housing bubble knowledge.

Enough to Make You Sick?

Those interested in epidimiology and urban economics should check out this article by Helen Epstein which was published in the New York Times in 2003. Epstein argues that the living conditions in urban areas are killing the people who live there. She states that deaths among the urban poor are not directly caused by common conclusions such as violence, malnutrition or extreme poverty - they are caused by a multitude of factors that can be attributed to one's living environment. Here is a sample from the article:

Something is killing America's urban poor, but this is no ordinary epidemic. When diseases like AIDS, measles and polio strike, everyone's symptoms look more or less the same, but not in this case. It is as if the aging process in people like Beverly and Monica were accelerated. Even teenagers are afflicted with numerous health problems, including asthma, diabetes and high blood pressure. Poor urban blacks have the worst health of any ethnic group in America, with the possible exception of Native Americans. Some poor urban Hispanics suffer disproportionately from many health problems, too, although the groups that arrived most recently, like Dominicans, seem to be healthier, on average, than Puerto Ricans who have lived in the United States for many years. It makes you wonder whether there is something deadly in the American experience of urban poverty itself.I felt that Epstein's article was pertinent to both last week's unit and the upcoming one, since poor public health in urban areas was an issue before the housing crisis (when the article was written) and continues to be one to this day. I would love to know if there has been a correlation between the number of home foreclosures and the number of diagnosed chronic diseases in the United States. (But then again, that number probably wouldn't be that accurate since people who can't afford their mortgage probably can't afford health insurance. Oh, America.)

Poverty and Foreclosure in Kalamazoo

Check out this report on poverty in Kalamazoo County. According to the survey, over half of the people in the city of Kalamazoo live below 200% of the poverty level, and one-third below 100% of the poverty level.

Part of the reason that so many people in Kalamazoo are living in poverty is, according to this data, the minimum monthly budget for a family of four is around $3,300, while both the U.S. Department of Health and Human Services and the Food Assistance Program in Kalamazoo put the number at only to $1,800 or $1,000, respectively. Kalamazoo's unemployment rate is also fairly high, at almost 11%.

We'll be talking about a lot of this data in class this week and how it has affected foreclosures in the area, but I wanted everyone to have the link to it to take a look because it has some pretty recent statistics (published in 2010).

US foreclosure, delinquency rates rise in minority communities

http://rt.com/usa/news/us-foreclosure-minority-communities/

Hello everyone, for this week, please focus on articles that relates to ethnic groups and foreclosures too. For instance, read the news article above and understand the amount of impact that the foreclosure has had on the ethnic groups.

"Foreclosures are increasing in 75% of America’s largest cities. The most devastated are the Black and Latino communities, where foreclosure and delinquency rates have almost doubled since Obama took office."

How come anglo people are not affected as much as other? What factors should we consider before making final judgments about this?

Banking Regualtions!! in the UK

|

Chancellor Alistair Darling has outlined his plans for reforming the regulatory system for the UK's financial system.

http://news.bbc.co.uk/2/hi/business/8104813.stmNew oversights will require banks to keep more cash in reserves and not leverage as much from their current debt levels. In England's tripartite system the Central Bank of England has checks in power with the Financial Services Authority and the Treasury. With the creating of new regulatory power the pendulum will shift more towards the FSA.

Is this a good idea? Should the United States Implement more regulations on our banks? Or is a Freer Market a better idea?? See end of Article for the U.S. perspective.

Sunday, April 10, 2011

A Reminder: Insights from 2nd Week

Could you all do this week's group a favor and comment with two things on this post:

1) An insight from class on Tuesday

2) An insight from class Thursday

This will help us decide what's important to the class as a whole so that we can structure the white paper around it.

Thanks for your help!

Is the US stuck in a second housing slump?

The economy at large is strengthening and consumer spending has increased, but the housing market has not bounced back. House prices have declined for a 6 straight month in the top 20 leading cities. Prices stabilized between spring 2009 and summer 2010, but are dipping once again.

According to the article, why are home prices dropping? Conservative attitude or the overall economy?

Does this agree or disagree with what we learned in Forclosure Nation?

http://www.pbs.org/newshour/bb/business/jan-june11/housing_03-29.html

According to the article, why are home prices dropping? Conservative attitude or the overall economy?

Does this agree or disagree with what we learned in Forclosure Nation?

http://www.pbs.org/newshour/bb/business/jan-june11/housing_03-29.html

Saturday, April 9, 2011

Value Place, Florida

I know it's not my week to post, but I thought this was interesting, kind of about the "new life" of those foreclosed on in my family's annual vacation spot, which made it even more relevant to me.

Thursday, April 7, 2011

Federal Progams Can Help People Avoid Forclosure

The Federal Government has several programs under hte Making Home Affordable inititative to help avoid forclosure that are only available to owners, not investeres. They includethe Home Affordable Refinancing Program (HARP) and the Home Affordable Modification Program (HAMP).

Nevada is the epicenter of the housing foreclosure crisis, where 1/79 houses end in mortgage default.

"A recent study found that more than half the Nevadans facing foreclosure didn't know anything about federal and state programs aimed at helping them. Furthermore, almost as many said their lenders were "not willing at all" to work with them."

Why haven't the people of Nevada taken advantage of these programs? What are your opinions of Federal Aide programs to help against foreclosure? Is this an ok way to spend tax payers dollars?

http://www.chicagotribune.com/classified/realestate/sc-cons-0407-save-home-20110407,0,5378502.story

Nevada is the epicenter of the housing foreclosure crisis, where 1/79 houses end in mortgage default.

"A recent study found that more than half the Nevadans facing foreclosure didn't know anything about federal and state programs aimed at helping them. Furthermore, almost as many said their lenders were "not willing at all" to work with them."

Why haven't the people of Nevada taken advantage of these programs? What are your opinions of Federal Aide programs to help against foreclosure? Is this an ok way to spend tax payers dollars?

http://www.chicagotribune.com/classified/realestate/sc-cons-0407-save-home-20110407,0,5378502.story

Why Homebuilding Doesn't Recover in 2011

Garza - Post #3

Really? Do you think so? Here's an article with analysis that probes the probability that homebuilding won't recover in 2011.

Now, even though it was published on November 3, 2010, it's still nice to think about it because according to the author, "Of course, even if there is growth in housing starts, what does it matter if those houses don't sell?"

Kalamazoo Foreclosure

http://www.foreclosure.com/search/MI_077.html

Since the top discussion right now has been on foreclosures in Kalamazoo, thought this website would be helpful to see how low foreclosed prices really are in our area. Along with prices of properties, the site also provides the numbers of short sales, bankruptcies, pre-foreclosures, foreclosures, sheriff sales and auctions.

Luxury or Need?

Here's an interesting article to think about as our discussion moves forward. The author of Foreclosure Nation treats home ownership as something that should be encouraged for all Americans. Paul Krugman examines that assumption here and talks about the Federal Government's attitudes towards home ownership. I'd like to know what everyone else thinks about the idea of home ownership as a part of the American Dream because in many cases, it isn't necessarily the best option for all citizens.

Intrest Rate Hike in Europe

http://www.washingtonpost.com/business/economy/european-central-bank-raises-interest-rate-over-inflation-fears/2011/04/07/AFtgWquC_story.html

The European Central Bank raised interest rates to 1.25%. Many analysis are saying that the United States Federal Reserve is behind in their contractionary policy and should hedge against inflation. Also, the fact that currently there is no room for the fed to lower interest rates should another crisis occur. If you know anybody considering buying a home (and can get a loan, a big if considering the loanable funds market) The time is now when rates are at historic lows and prices are currently in the gutter in terms the last 30 years approximately.

How do we as a class feel about increasing interest rates in the united states which will ultimately lead to higher interest rates for mortgages?

The European Central Bank raised interest rates to 1.25%. Many analysis are saying that the United States Federal Reserve is behind in their contractionary policy and should hedge against inflation. Also, the fact that currently there is no room for the fed to lower interest rates should another crisis occur. If you know anybody considering buying a home (and can get a loan, a big if considering the loanable funds market) The time is now when rates are at historic lows and prices are currently in the gutter in terms the last 30 years approximately.

How do we as a class feel about increasing interest rates in the united states which will ultimately lead to higher interest rates for mortgages?

Outline for white paper

Also, check out this link to the outline for the class white paper. Add to it and give us your feedback on what you think is important.

Thanks!

Thanks!

Change in perception, The 30 year mortgage

http://www.youtube.com/watch?v=5y8fNbM0-t0

The rule of 72's (read below for simplified definition and explanation of the time value of money).

http://calrealestatefinance.com/?p=15

When a loan is taken out for double the amount of time (from 15 to 30 years) generally the borrower assumes stability for that period of time, and in this case that denotes borrowers expectations that they will be able to fulfill the terms of the loan. In the months before the bubble burst borrowers were signing up for mortgages that had interest only options....... this means that the borrower is essentially paying nothing on principle and will accrue no equity over the life of the mortgage. Also it means that the bank owns your house after the 30 years is up or the terms of the loan are fulfilled. (30 years of renting)

The lender charges interest on principal for every year of a mortgage and some times continuously or compounding every minute.

The interest is charged to remaining principal (or the amount taken out originally say 300,000 would be the principal of a 300,000 mortgage) of that loan. In a mortgage the borrower pays mostly interest in the beginning of the loan and eventually pays mostly principal towards the end of the loan. AKA the bank gets its return on investment first and then you get to pay back what you borrowed.

So, the change in expectations or the bursting of the bubble in terms of the value of homes has lead to a more savvy consumer. I like to think that the guy in the 30 year mortgages are Satan as the new savvy consumer...

What do you think about the changes in mortgages, length (15 vs 30 years), terms (interest only adjustable rates ect), lending practices (commission for the amount of mortgages closed for loan mortgage brokers), and finally homeowner expectations (of stability and future home values)????

The rule of 72's (read below for simplified definition and explanation of the time value of money).

http://calrealestatefinance.com/?p=15

When a loan is taken out for double the amount of time (from 15 to 30 years) generally the borrower assumes stability for that period of time, and in this case that denotes borrowers expectations that they will be able to fulfill the terms of the loan. In the months before the bubble burst borrowers were signing up for mortgages that had interest only options....... this means that the borrower is essentially paying nothing on principle and will accrue no equity over the life of the mortgage. Also it means that the bank owns your house after the 30 years is up or the terms of the loan are fulfilled. (30 years of renting)

The lender charges interest on principal for every year of a mortgage and some times continuously or compounding every minute.

The interest is charged to remaining principal (or the amount taken out originally say 300,000 would be the principal of a 300,000 mortgage) of that loan. In a mortgage the borrower pays mostly interest in the beginning of the loan and eventually pays mostly principal towards the end of the loan. AKA the bank gets its return on investment first and then you get to pay back what you borrowed.

So, the change in expectations or the bursting of the bubble in terms of the value of homes has lead to a more savvy consumer. I like to think that the guy in the 30 year mortgages are Satan as the new savvy consumer...

What do you think about the changes in mortgages, length (15 vs 30 years), terms (interest only adjustable rates ect), lending practices (commission for the amount of mortgages closed for loan mortgage brokers), and finally homeowner expectations (of stability and future home values)????

Insights from Class This Week

Could you all do this week's group a favor and comment with two things on this post:

Could you all do this week's group a favor and comment with two things on this post:1) An insight from class on Tuesday

2) An insight from class today

This will help us decide what's important to the class as a whole so that we can structure the white paper around it.

Thanks for your help!

Property Stripping: Big Problem in Real Estate

http://www.parsonsgroup.com/home-stripping-crimes-on-the-rise-as-foreclosures-increase/

The article tells the stories slightly different than what I have heard in my community with short-sales, but it’s the same concept. The situation I have heard this that people were buying or building homes they could not afford using a mortgage. Once they buy or start building their nice house, they buy the best hard wood floors/ expensive tile patterns/ granite countertops /etc to match their nice house. People justified their big spending, because they saw these luxury products as an investment in their property that will increase the property value if they ever want to sell their house in the future. A few years or so down the line, they can’t keep up with their mortgages and the house is foreclosed. Now picture yourself in this situation. If a builder/contractor offered you thousands of dollars to have their workers strip all those luxury goods out of your house, it makes sense to you since you are in debt and the bank is going to take you home anyway. As the debtor to bank, you see not stripper your property as letting the bank take even more of your money. What the contractor/builder will then do is hold on to the materials they stripper and resell it to the next person who buys the house since everything already matches the measurements and style of the house.

Complete Fraud!

http://reitwrecks.com/2010/03/next-wave-of-the-housing-crisis-much-more-pain-in-2010-2011.html This is kind of a scary article as we read and hear reports about how the economy is starting to recover. I think we are getting close to watching the toilet flush again......

Wednesday, April 6, 2011

Accountability anyone?

http://www.youtube.com/watch?v=coSn3iCTbBw&feature=autoplay&list=PL9D5372719B1A3FC6&index=4&playnext=2 The opinions about this video can go either way. Most people dont bring an attorney to a mortgage closing, but where is the accountability of the homeowner? Who knows better then they do what they can or cannot afford on a monthly basis. This video illustrates the lack of self awareness that pervades our society. That many people now sign mortgages without even reading the paperwork blows me away. If you dont understand, you shouldnt sign. Greed overcomes common sense more often than you might think.

Proof of Fraud

http://www.youtube.com/watch?v=6khYSTqHrqM&feature=BF&list=PL9D5372719B1A3FC6&index=2 This is a link to a video that ties in nicely to chapters 4 and 5 of the book. If it doesnt make you angry, then something is wrong......

Tuesday, April 5, 2011

Turn your house into a billboard, get free mortgage

Garza - Post #2

Ok. Wow.

I never thought about this solution before, but it looks like a really nice tradeoff. Adzookie says that it will pay the house owner's mortgage every month for as long as the home styas painted.

Think about this for a sec. This could be an interesting strategy for the firms to use and actually give them leverage in the competition. Nike, Sprint, and etc... Advertisements make it possible for the consumers to know what's in the market and what goods and services are there. It's a great way to draw our attention to a certain product.

Well, if I'm in a pickle, I think I'll do that for a while. How about you?

How to Add This Blog as an RSS Feed to Your HootSuite Account

1) Copy this link, which is the RSS feed for our blog: http://urbanmesses.blogspot.com/feeds/posts/default?alt=rss

2) Go to HootSuite.com and click "Settings" on the left-hand side (the icon that looks like a gear).

3) Click "RSS/Atom" and click "Add New Feed" at the bottom of the page.

4) Enter that link above and choose your settings. Be sure to select a profile to send your feed to (your Twitter would probably be the most logical).

5) Click Save Feed and you're set! It may take a while for the RSS feed to import to your Twitter HootSuite feed.

Send me an email if you have any problems at k09bc03@kzoo.edu!

Link to Social Media How to Guide

Click Here!

and be sure to contact Bridgett or Laura for questions!

and be sure to contact Bridgett or Laura for questions!

Link to White Paper One

Here's the link to the white paper part one!

https://docs.google.com/document/d/1LAKp6WhNckrkB-sO4zmBeCccD55nU_-BfZqyKSVWwJ4/edit?hl=en&authkey=COqrv_gI

https://docs.google.com/document/d/1LAKp6WhNckrkB-sO4zmBeCccD55nU_-BfZqyKSVWwJ4/edit?hl=en&authkey=COqrv_gI

The Rush to Build Urban Grocery Stores

The Urban Land Institute, a major urban planning organization, has an article about increasing urban gentrification (think the opposite of the White Flight) and the demand for urban grocery stores. Smaller grocers are out and big, chain companies are fighting to get into this market. Minneapolis, my hometown, has medium sized grocers popping up everywhere, with a large Target in the heart of the city.

I encourage you to read the article. Its well written and explains what's going on today.

What are the implications of increased commercialization in urban centers? Is this good or bad for the city?

I encourage you to read the article. Its well written and explains what's going on today.

What are the implications of increased commercialization in urban centers? Is this good or bad for the city?

Week One reading summary insights

The first week's reading served two purposes. The first was to introduce you to the basics of foreclosure and banking. The Olefson book argues that our debt-oriented culture created an environment where the foreclosure crisis was all but inevitable. Comments and insights please on the chapters for the week.

Then the two articles have two very different purposes. The Tiebout article is a classic in urban theory. It provided the theoretical rationale for the type of fragmented local government finance seen in the United States. The second reading concerns cities in the nineteenth century. I asked you to read it because the authors painstakingly gathered data on urban finances and discovered that a long-held theoretical belief was wrong. Good data should always trump theory, or, at the very least, lead to changes in theory. Comments and insights?

Then the two articles have two very different purposes. The Tiebout article is a classic in urban theory. It provided the theoretical rationale for the type of fragmented local government finance seen in the United States. The second reading concerns cities in the nineteenth century. I asked you to read it because the authors painstakingly gathered data on urban finances and discovered that a long-held theoretical belief was wrong. Good data should always trump theory, or, at the very least, lead to changes in theory. Comments and insights?

Monday, April 4, 2011

Banks Offer Own Mortgage-Servicing Plan

This may be interesting to follow. The nations five largest banks have sent a proposal to government officials. It would be interesting to see if it’s possible to find the document that was sent and what the government’s response will be.

60 Minutes article on Foreclosure

This article was very interesting because it talks about the fraud that goes on with the banking system and their paperwork dealing with foreclosure. Also there is a video clip from the episode online at 60 Minutes' website which gives an overview of what is happening with fraudulent paperwork.

http://www.cbsnews.com/stories/2011/04/01/60minutes/main20049646.shtml?tag=contentMain;cbsCarousel

"The Giant Pool of Money"

Here's an episode from NPR's "This American Life" hosted by Ira Glass on the mortgage crisis. The program provides an intimate, personal look some of the people who initiated the financial programs that caused the mortgage crisis and a portrait of those whose lives were changed forever by the collapse of the housing market. With all the CDOs, MBSs, and ARMs, the human element of this crisis can be lost. Glass's reporting makes this moment in history personal and helps you understand it through individuals, not acronyms.

Sunday, April 3, 2011

Americans clueless on credit scores

Garza - Post#1

When we hear about credit score and stuff about finance, we tend to ignore it and move on with our lives. Look, if you don't know what credit score and stuff about finance are, you are in trouble because you are giving leverage to the financial institutions like bankers so they can make more profit out of you. There's this saying from this book, called Foreclosure Nation: The less you know, the more you pay. So what's going on here is that we are having a breakdown in consumer education, according to Linda Sherry, spokeswoman for advocacy group Consumer Action, and if we want to live happy lives with wonderful homes, then I suggest that you understand everything you need to know about credit score, debt, and spending too.

First, let me ask you some questions:

- Do you (and your parents) really know what credit score is?

- Do you only have 1 credit card and hardly use it? (If not, then please read this article:

http://articles.moneycentral.msn.com/Banking/CreditCardSmarts/1In7AmericansCarries10CreditCards.aspx)

- Do you even keep the receipts and write it down in your checkbook?

- Do you tend to look at your checkings/savings once per week and make sure that you don't go overboard?

1. If you answer "no" to all, then you are very clueless about your debts and spending.

2. If "yes" to all, then you're awesome. :)

So lack of education in finance and spending has a lot to do with foreclosure and its impact on us.

Some advice for homeowners: Even though that you have great credit and income, it doesn't mean that you can take out many mortgage loans. Yes, I understand that the higher the credit score, the better the mortgage deal, but think about it. Do you really want to be paying a lot of money until you die? If something happens to you or your family and you start to be behind with your mortgage payments, how will you pay for the mortgage?

Check out this article about how foreclosure affects your credit score.

Yes, this might be "common sense," but a lot of people aren't getting it at all.

Subscribe to:

Posts (Atom)